Watermelons, more watermelons

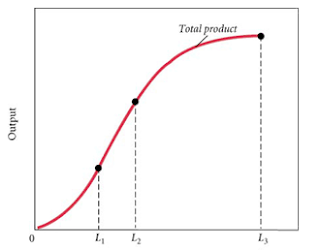

If we could plot "global anxiety over the end of times" (the end of human times, that is) on a time series graph, I would say that now we would be at --or close to-- an all-time high. Typhoon Yolanda's epic size and strength is indeed a reminder of how insignificant we are, which definitely does not help to calm that feeling of impending doom. End-of-the-world anxiety takes different forms. Economically speaking, the specter deflation is one of them. The New Normal , or the idea that we have reached a point from whence we will never achieve the growth rates of yesteryear is another. This idea, defined as a statistical regime change, can also be described as an inflection point, or the point at which the speed of growth decelerates going forward. In other words, the point at which the second derivative of GDP turns negative. The New Normal : The second derivative (the slope's rate of change) turns negative at L 1 The reason this inflection point occur...